Why South Korea’s market is flying

South Korea’s stock market has surged on the back of memory chip strength, pushing the IKO ETF to extraordinary gains in early 2026.

The South Korean stock market has been absolutely flying.

As I write, the IKO ETF, which is the iShares MSCI South Korea ETF listed on the ASX, is up 119% in a year, most of which has come in the last six months, with the ETF up 91% from the September low and up 52% from late December. As I write, it has just peaked at A$212, having risen from A$111 in September 2025.

We are not about to buy it, but it’s an interesting analysis to work out why this has happened. For next time.

This is the description.

.png)

This is our ETF SNAPSHOT.

.png)

What the IKO ETF actually holds

The ETF represents the South Korean KOSPI Index, which has 81 stocks in it, and the ETF currently has AUM of (just) $172m. That’s not very much. Out of 427 ASX-listed ETFs, this is number 229 by size.

It is entirely an equity-based ETF. Here are the top 20 underlying stocks. Korea is an interesting market, with a few companies like Samsung and Hyundai having multiple entities. So it is a very concentrated ETF.

.png)

As you can see, the index is dominated by two companies: Samsung Electronics (KRX: 005930), which is 28% of the ETF (35% of the ETF is Samsung-listed entities), and 24% is SK Hynix (KRX: 000660). To understand the ETF, you need to understand these two companies.

Samsung Electronics engages in the manufacturing and selling of electronics and computer peripherals. The company operates through the following business divisions: Device Experience (DX), Device Solutions (DS), Samsung Display (SDC), and Harman. The DX division offers televisions, monitors, refrigerators, washing machines, air conditioners, smartphones, network systems, and computers. The DS division deals with semiconductor components including DRAM, NAND Flash, and mobile APs. The SDC division provides OLED panels for smartphones. The Harman division consists of digital cockpits, car audio, and portable speakers. The company was founded on January 13, 1969, and is headquartered in Suwon-si, South Korea.

SK Hynix engages in the manufacture and sale of semiconductor products. Its products include dynamic random access memory (DRAM), flash memory, complementary metal oxide semiconductor image sensor, and others. The company was founded on October 15, 1949, and is headquartered in Icheon, South Korea.

A semiconductor proxy in disguise

Now look at the sector breakdown in the SNAPSHOT and you’ll see that 50% of the index and ETF is in the IT sector. 10% is industrials (shipbuilding, machinery, construction), 10% is financials (banks, insurance and Mirae), 10% is consumer discretionary (includes Hyundai and KIA), so what we have here is a proxy for semiconductor exposure through memory chips and semiconductors, as well as display panels. Plus others (which rather mellows it out risk-wise).

So the main drivers include:

- If Samsung Electronics moves, the KOSPI moves.

- If memory prices move, the KOSPI moves.

- If global trade weakens, the KOSPI feels it because it is an export-led economy.

- Another factor is tariffs.

- The other factor is the currency. The KRW (Korean won) is important to exports and to the price of the ETF listed in Australia. A weak won is great for the competitiveness of exports. The main driver of this weakness has been lower interest rates (similar to Japan) relative to Western counterparts.

.png)

It’s all about memory chips

In the short term, the performance of the individual biggest is in this table – Korean stocks have been flying:

.png)

It’s all about memory chips. See this chart – it explains everything.

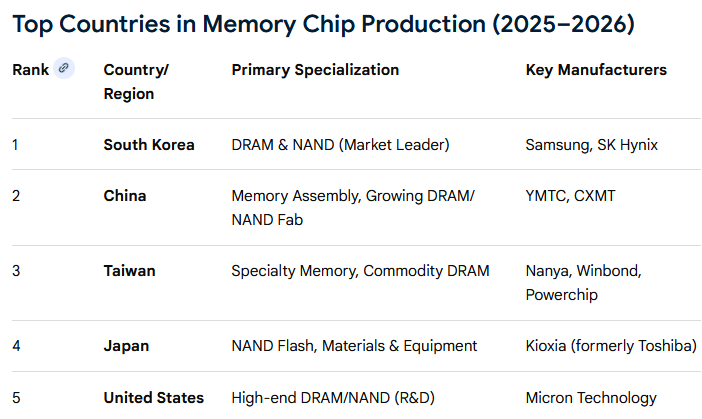

The two top stocks in Korea are in the box seat to provide memory chips. They, like the semiconductor stocks, are the picks and shovels of the data centre build-out. Samsung and SK Hynix control over 70% of the global DRAM market, with Micron (USA) also holding a significant share. Samsung leads in NAND production (NAND is used in smartphones, laptop SSDs, tablets and cameras), followed by SK Hynix and Kioxia (Japan). China is expected to challenge Korea and Taiwan in total IC wafer capacity by 2026, though still hampered by equipment restrictions for advanced chips.

Valuations raise an obvious question

The IKO ETF is a proxy for the global data centre build. What is interesting is that next year’s PE for Samsung Electronics is 9.3x, and for SK Hynix it’s 5.8x. Are we missing something? Finally, a couple of tech stocks that are not expensive.

.png)

On those PEs, it might continue to run. The chart says we’ve missed it. We would need to know a lot more about Samsung and SK Hynix to buy it (charts have gone parabolic). And we don’t.

If you hold it, hold it. Until it cracks. Hasn’t cracked yet.