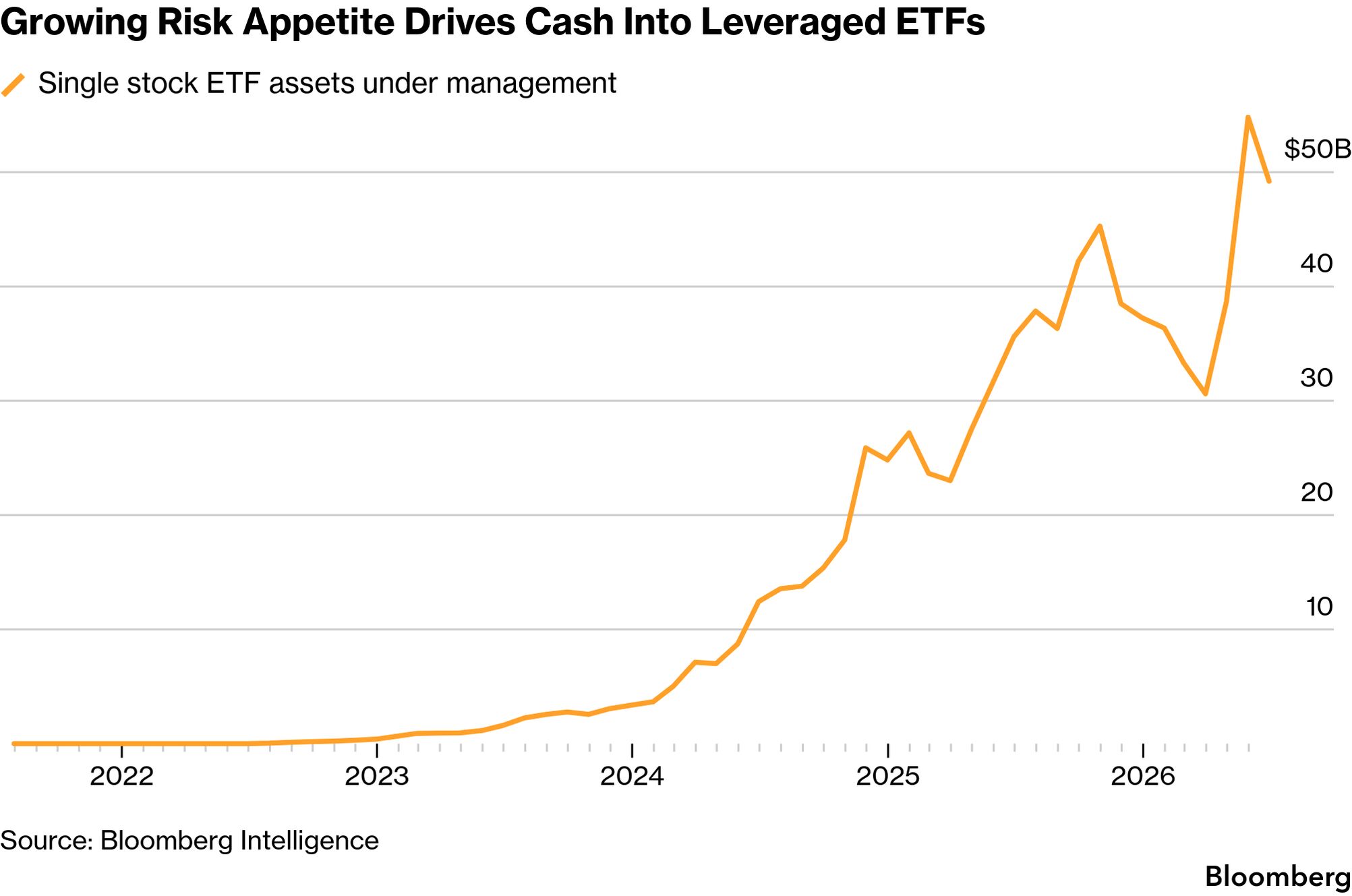

The hidden danger of leveraged ETFs

Leveraged ETFs crashed the KOSPI and now AI spending is raising the same uncomfortable question: what happens when the bill comes due?

I think that ETFs are a wonderful invention. They enable retail investors to get exposure to international markets, sectors and themes. Brilliant stuff and obviously has been a huge success. But success has many fathers, and huge success has many players. Competition is fierce for ETF dollars. These fund managers want your money. The fees are low (part of the attraction), so you need lots of dollars to make it work. The same infrastructure is required to manage $1bn as $100m. The same models and mechanisms.

But competition can be fierce. As a result, they come up with ever more exotic themes, ever more exotic sectors and, worst of all, leveraged ETFs. These can include SNAS or LNAS. These offer leverage of around 2–2.5 times the index move. But when things get weird, worrying is the level of leverage that some providers offer in other markets. Korea is a case in point.

When leverage turns against you

It is only fabulous when the market goes up, and leverage magnifies the underlying index moves. It is a bit like an option position. As the market goes up, the sellers of these ETFs are getting shorter and shorter due to the leverage. So they have to keep buying to stay hedged. This pushes the market higher and higher. The trouble is that when things unravel, they tend to unravel quickly. The market makers get longer as it goes down, and so have to rebalance and sell. Couple that with the pain from investors, and it can cascade lower.

The Korean market has a huge level of leverage with new products in Samsung and SK Hynix. That is why we saw a 10% fall in the KOSPI yesterday. It feeds on itself. Even the regulator that approved these highly leveraged products has said maybe it wasn’t his greatest idea! That is a stark admission. That is something that is supposed to be said in an “inside” voice!

Nomura estimates leveraged ETFs now broadly generate about $9 billion of rebalancing demand for every 1% move in the market.

Korea set off the US sell-off. Everything is connected after all. At their May launch, the 16 ETFs tracking the chipmakers in Korea had combined assets of US$3bn. To date, these have ballooned to more than US$9bn.

What is also troubling in all this leverage is that they are very popular with retail investors who may not be that experienced in risk management. Just rolling the dice to get rich or die trying! Up until recently, it has worked. Until recently.

Leverage is a wonderful thing when it is going well. When it turns, it can be a very sub-optimal experience. And it can unwind the popular trades very quickly. That’s what we are seeing at the moment. Those crowded trades unwound at breakneck speed.

The real cost of the AI boom

I wrote yesterday about the AI issue. That is the cost of it. It is huge. There is probably going to be a trillion dollars chucked at it this year. That requires a payback. Companies that embrace AI have to see the returns because it is expensive.

And do you need a hammer gun to knock in one nail? Does “free” ChatGPT do the job, or do you need advanced Claude models to run your business? And if you are paying a fortune for your AI bots and models, do you need humans? Low value human capital. Like the reverse of the Taco Kid ad. You can’t have both. What is the point? It is like buying a designer dog and then wishing you had a rescue one! If you only want one dog, that is. The goal is to save money and be more productive.

The big tech stocks have gone from being massive holders of cash to issuing debt and equity to pay for all the spending! That is a significant change to the models. From cash hoarders to Shirley Bassey stocks. Big spenders.

I use ChatGPT; I am not a complete Luddite, but for my requirements, it does a pretty good job. I am not into just posting AI stuff. It is nice to think about things.

What does compute actually cost?

The concern I have is how much does “compute” cost? Does it just become a commodity? The big spenders want you to use it more and more, in more and more sophisticated ways. Tokens, tokens everywhere and not a brain to think!

If you invest $1 trillion, you would like to see a return. A pretty good one. Especially as you are not sure how long the chips will last and how quickly you will have to upgrade. Then there is the question of open-source Chinese AI models, which are vastly cheaper and sometimes free. Will the Chinese do to the tech models what they have done to German car makers? Going the way of the Dodo!

Does anyone know the cost of a “compute token” in a year? What about five years? As they say, investing in resource stocks is risky because you don’t know what iron ore prices will be in five years. Yet they are still investing $1 trillion a year! Is this another period when the markets have lost their minds? Irrational exuberance. Vale Greenspan. He called it.